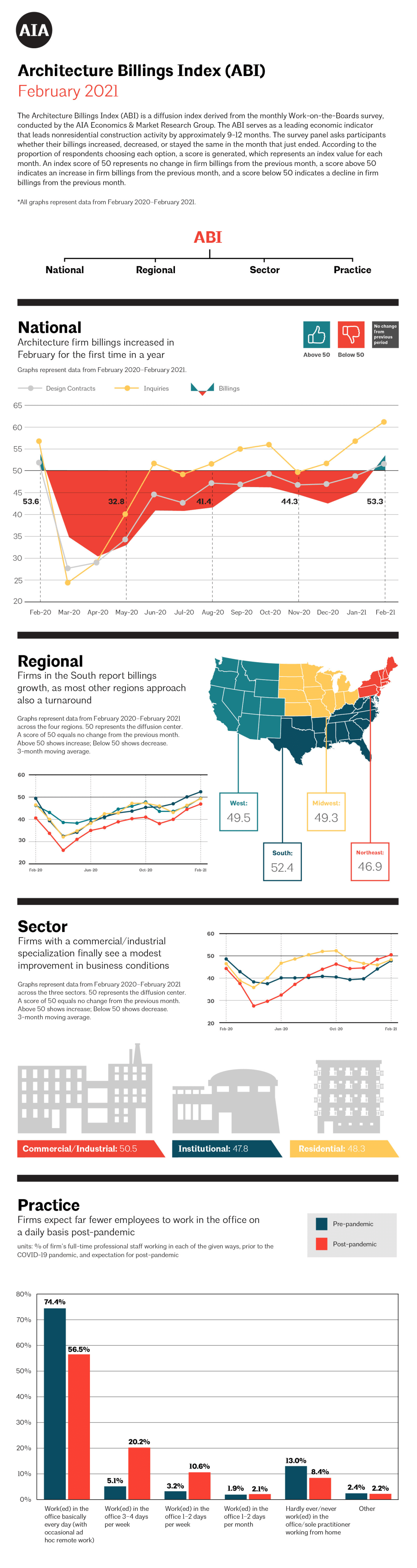

Architecture firm billings returned to the positive side in February for the first time in a year, with the AIA’s Architecture Billings Index (ABI) score climbing by more than eight points from January to a score of 53.3. Hopefully, this is the start of a more sustained recovery, however, it is possible that scores continue to bounce above and below 50 for the next few months, as recoveries often move in fits and starts. Indicators of future work also returned to the positive side this month, with inquiries climbing above 60 for the first time in nearly two years, and the value of new design contracts returning to growth for the first time since February 2020. All of these indicators are encouraging signs that business is beginning to return to many firms that had been struggling, and should continue to improve as the pace of vaccinations accelerates and the impact of the latest government stimulus continues to spread.

Firms located in the South region of the country reported billings growth for the second consecutive month in February, while firms located in the West and Midwest saw only small declines, and look likely to return to growth soon themselves. Conditions remained softest at firms located in the Northeast, but the pace of the decline in firm billings slowed for the third month in a row. And firms with a commercial/industrial specialization, among the hardest hit by the pandemic, reported a very modest improvement in their business conditions this month, as industrial activity remains strong, and some restaurants and stores began to reopen. In addition, the pace of the decline in billings slowed at both multifamily residential and institutional firms.

Encouraging signs in architecture and the broader economy

Conditions continued to improve across much of the broader economy in February as well. Nonfarm payroll employment grew by 379,000 new positions, with employment in leisure and hospitality adding 355,000 positions alone. However, construction employment declined by 61,000 positions, likely due to the severe winter weather across much of the country. Architecture services employment added 700 new positions in January (the most recent data available), and has now regained 45% of the jobs that were lost during the pandemic. Overall, the architecture industry is faring modestly better in their recovery than overall national employment – employment for the sector is currently 4.4% below its pre-pandemic peak, while national employment is still down by 6.2%.

The University of Michigan’s Index of Consumer Sentiment also showed encouraging signs in its latest release in early March, rising to its highest level in a year. Although the index is still 6.8% below its level a year ago, consumer optimism about prospects for the national economy increased, and strong growth in consumer spending is expected in the months ahead. The one lingering issue is personal finances, where ongoing consumer concern did not improve in this release.

A changing work landscape

This month’s special practice questions asked architecture firms for an update on their post-pandemic office space needs and plans for remote work for employees in the future. Overall, responding firms reported that a broad majority of their full-time professional staff (74%) worked in the office basically every day pre-pandemic, with only occasional ad hoc remote work. Firms expect this share to decline dramatically, predicting that just over half of their employees (57%) will work in the office every day post-pandemic. In addition, firms expect that the share of staff working in the office 3–4 days a week will increase from 5% to 20%, and the share of staff working in the office just 1–2 days a week will increase from 3% to 11%.

Following these expected changes, firms indicated that they plan to be broadly supportive of remote work requests in the future. Only slightly more than one quarter of firms (28%) anticipate that they will limit or restrict remote work post-pandemic, with just 7% indicating that they will completely prohibit it in most cases. On the other hand, 62% of firms say that they will be flexible with remote work requests based on individual employee needs, while 4% will encourage remote work, and 3% will require it in most cases.

Based on these projected new work patterns, just over one third of firms (34%) anticipate that they will need less office space post-pandemic, with 6% expecting that they will no longer have any permanent office space and their entire staff will telecommute permanently. This share was highest for small firms and for firms with a multifamily residential specialization, where 20% and 13%, respectively, expect staff to work from home permanently post-pandemic. But by and large, most firms (56%) anticipate that their office space needs will remain the same, and that even with fewer employees in the office on a given day, they will need the extra space to maintain social distancing practices. In addition, 7% of firms plan to increase their office space post-pandemic.

This month, Work-on-the-Boards participants are saying:

“Increase in inquiries and workload for the near term. We hired three staff persons in the last three weeks. The question is whether this is a blip or indicative of a longer-term trend.”—21-person firm in the South, commercial/industrial specialization

“The market seems to be picking up, but I am concerned that material costs and inflation are going to stall things.”—5-person firm in the Midwest, institutional specialization

“A lot of proposals out, but clients are slow giving the go ahead.”—44-person firm in the Northeast, residential specialization

“Conditions are slow. While there is activity, it takes much longer to close a deal, and substantially longer to process through governmental jurisdictions.”— 30-person firm in the West, institutional specialization